What is Mortgage Protection ?

Only Death & Taxes Are Certain

Benjamin Franklin

Mortgage Protection Insurance (MPI)

is an insurance product designed to alleviate the financial burden on families when a primary breadwinner passes away or becomes disabled. It ensures that the mortgage remains paid off, helping beneficiaries retain their home without the pressure of monthly payments. Below is a detailed overview of MPI, covering its operation, coverage, comparisons with other insurances, benefits, and drawbacks.

How It Works

Mortgage Protection Insurance operates by directly paying the outstanding mortgage balance to the lender upon the policyholder’s death or qualifying disability. Unlike traditional life insurance that pays a sum to the beneficiaries, MPI redirects any payouts exclusively to the mortgage lender. This mechanism is intended to provide financial security to the mortgage lender while also ensuring that beneficiaries can avoid the stress of managing large debts. By securing the loan amount, policyholders can bolster their family’s equity in the home, reducing the likelihood of foreclosure.

What It Covers

Typically, MPI covers the principal and interest of the remaining mortgage balance. However, it generally excludes ancillary fees such as property taxes, homeowners insurance, or homeowners association (HOA) dues. For comprehensive coverage that includes these additional payments, policyholders may opt to add riders to their MPI policy, allowing them to cover more financial responsibilities associated with homeownership.

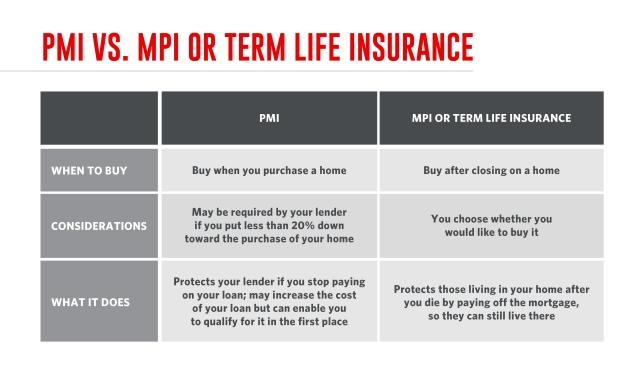

Comparison with Other Types of Insurance

While MPI shares similarities with life and disability insurance, it is often perceived as more accessible since it typically doesn’t require medical examinations for policy approval. This absence of underwriting makes MPI an attractive option for individuals with pre-existing health conditions or those engaged in high-risk occupations. Additionally, it should not be confused with mortgage insurance, which only protects the lender’s interests in case of payment default and does not offer death benefits to the policyholder’s family.

Benefits of MPI

One of the primary advantages of MPI is the peace of mind it offers to families, knowing their mortgage obligations will be handled in case of an unforeseen event like death or disability. This assurance can help families maintain their home and avoid financial strain during difficult times. Lenders support the concept of MPI as well since it significantly lowers the risk of foreclosure, thereby securing their investment.

Drawbacks of MPI

A notable drawback of MPI is that as the mortgage balance declines due to payments over time, the insurance payout encapsulated in the policy also reduces, even though the premiums typically remain constant. This diminishing benefit might lead to a situation where policyholders pay more in premiums than they would receive in benefits later in the loan term. Additionally, if the beneficiary requires funds for expenses beyond the mortgage, MPI falls short as it does not provide a lump-sum benefit to cover other financial needs.

In Summary

Mortgage Protection Insurance is a unique type of life insurance designed primarily to relieve the financial burden associated with mortgage payments in the event of death or disability. While it offers specialized benefits and ease of access, potential policyholders should carefully evaluate the coverage limits and costs involved to determine if it aligns with their long-term financial strategy.